When Congress passed the No Surprises Act (NSA), the goal was clear: protect patients from unexpected out-of-network bills and shift disputes over payment into a neutral arbitration process. At the center of this process is the Qualifying Payment Amount (QPA)—a benchmark meant to anchor payment fairness.

But two years in, the numbers tell a different story: rapidly rising disputes, growing legal backlash from payers, and a widening rift between providers and health plans over what constitutes a “fair” price. The QPA isn’t solving the problem—it’s exposing it.

Using the Q2 2024 Federal Independent Dispute Resolution (IDR) dataset, we explore how the QPA is working in practice—what’s being disputed, who’s winning, and whether the system is driving us toward or away from true price transparency.

What Is the QPA—and Why Does It Matter?

The QPA represents the payer-calculated median in-network rate for a service in a given geographic region. It’s meant to serve as the anchor point for out-of-network payment negotiations and arbitration. Health plans are required to disclose the QPA when they issue initial payment, and providers can choose to accept it or initiate Independent Dispute Resolution (IDR).

In theory, this creates a neutral, data-backed foundation for fair payments. In practice, it’s led to deep skepticism—especially from providers who have no visibility into how QPAs are calculated and who routinely see QPAs that fall far below what they consider market rates.

Disputes Are Surging

Between January 1 and June 30, 2024, disputing parties initiated 610,498 disputes through the Federal Independent Dispute Resolution (IDR) process.

That’s a 56% increase compared to the number of disputes submitted in the last six months of 2023, indicating a continued—and accelerating—trend of using arbitration as the default resolution path rather than the exception.

This dramatic growth reflects deep dissatisfaction with initial payment amounts and a systemic breakdown in pre-arbitration resolution. Instead of a safety net, the IDR process is becoming a frontline strategy.

Which Services Are Disputed Most Often?

According to the Q2 2024 data, the most commonly disputed services include a mix of emergency care and imaging services—areas where patients typically don’t choose their provider and services are frequently rendered out of network:

- 71045 – X-ray of chest, 1 view

- 74177 – CT scan of abdomen and pelvis with contrast

- 99283 – Emergency department visit, low complexity

- 99284 – Emergency department visit, moderate complexity

- 99285 – Emergency department visit, high complexity

These services are high-volume and high-stakes, particularly in emergency departments where provider networks often break down at the point of care.

Who’s Winning—and by How Much?

Based on Q2 2024 outcomes were heavily skewed in favor of providers:

- Providers won 83% of arbitration cases

- Health plans won just 17%

- Split decisions were <1%

This data suggests that arbitrators are consistently unconvinced by the payer’s QPA-based offer—particularly when the provider can make a strong case for clinical complexity, market rates, or specialty justification.

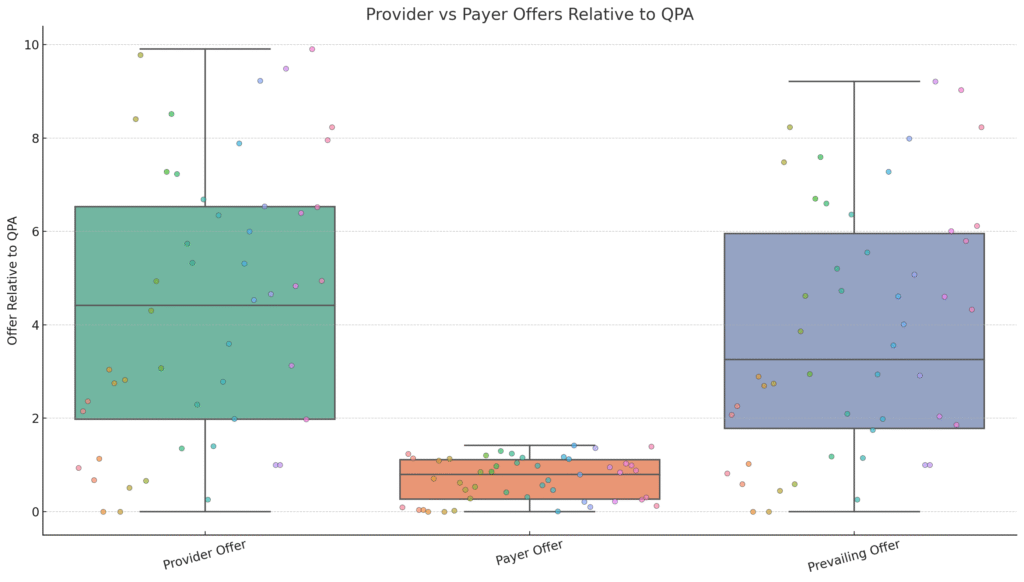

But the bigger story is how much is being awarded. On average:

- Providers submitted offers at 276% of the QPA

- Health plans offered 130% of the QPA

- Prevailing awards averaged 257% of the QPA

This suggests that arbitrators are not merely ignoring the QPA—they’re choosing values far above it, aligning closely with provider requests. This calls into question the practical value of QPA in dispute resolution. If it’s rarely accepted as “reasonable,” can it still serve as a fair reference point?

Post-Award Battles: Now the Pushback Begins

Arbitration was supposed to bring finality. But now, post-award enforcement disputes are emerging as a second battleground.

- Blue Cross Blue Shield of Georgia (BCBSGA) has challenged multiple awards in federal court, arguing that arbitrators are disregarding legal criteria and favoring inflated provider rates.

- Aetna sued Radiology Partners, alleging the provider group used IDR to extract “excessive” reimbursements by manipulating documentation and avoiding network negotiations.

These cases illustrate a deepening divide over what constitutes a fair market rate—and now health plans are turning to the courts to resist arbitration outcomes they believe are distorting pricing rather than correcting it.

From Protection to Inflation: Are Arbitration Incentives Driving Up Costs?

The No Surprises Act’s arbitration model was designed to protect consumers—but it may be undermining price discipline across the market.

- Providers have strong incentive to reject QPA offers and pursue arbitration, where the data shows they are likely to win—and win big.

- The QPA remains opaque, calculated solely by payers without external validation.

- There is little market correction, since arbitration decisions are not binding across claims and do not feed back into QPA calculations.

As a result, provider revenue is increasing for some, but member costs may follow—especially in self-funded plans where arbitration-driven overpayments can ripple through premiums.

Conclusion: A Broken Middle Ground

The No Surprises Act has brought necessary protections to consumers and some structure to out of network billing. But the QPA, while central to the process, hasn’t delivered on transparency.

It’s a benchmark without visibility, a number that’s supposed to create fairness but often perpetuates conflict. If we want real transparency in healthcare pricing, we need more than payer-defined medians—we need:

- Shared methodology

- Publicly auditable benchmarks

- Market-wide access to the data used to calculate QPA

Until then, the battle over what’s “fair” will keep moving from exam rooms to courtrooms—with price transparency still just out of reach.